Grade A commercial office spaces in India have transitioned to a new paradigm where they are more than just places of work; they have evolved into high-quality experiential ecosystems where individuals can seamlessly blend work, leisure, and lifestyle activities. This transformation is evident in the integration of various amenities into office environments, including sports facilities, restaurants offering culinary delights, premium shopping options, and other conveniences. Occupiers now prioritize green buildings and spaces that incorporate lush landscapes and open areas into their parks, enabling natural lighting and fostering a connection with nature enhancing wellness and productivity.

The resultant uptick in demand for Grade A assets is evident, with institutionally managed office spaces capturing significant percentage of the demand.

Return to office becoming mandatory

Both occupiers and employees have come to recognize and appreciate the advantages of inperson interaction. As a result, there is a significant push from senior leadership to encourage employees to return to the office few days a week with some offices ending remote work completely and making it mandatory to be in office. The aim is to reintroduce employees to an environment that promotes collaboration, enhances innovation, and bolsters productivity. Consequently, there is a heightened emphasis on occupying premium Grade A office ecosystems.

Office demand recovery propelled by:

- Strong demand from Global Captive Centers (GCCs) and domestic enterprises on the back of growing economy and

availability of skilled talent

- Companies starting to call back employees to office

- Preference of occupiers to operate from secured office environments with adequate health, safety and

wellness protocols

- Shift from strata sold assets to quality, single-owner Grade A properties

- Rise in demand for campus-style developments

Presence in the best performing micro-markets

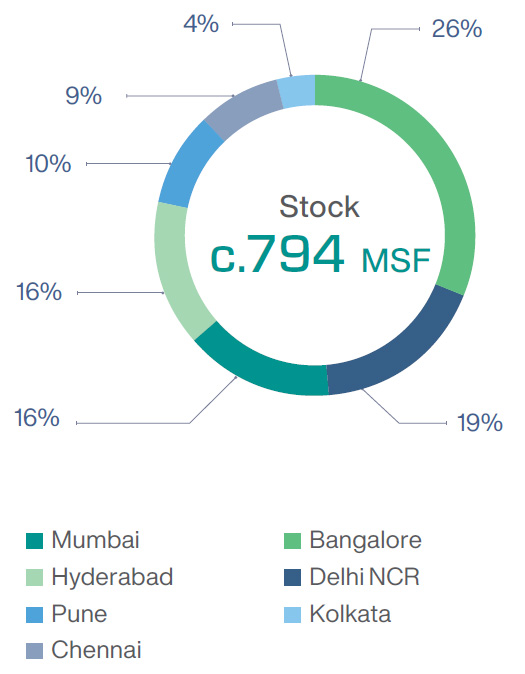

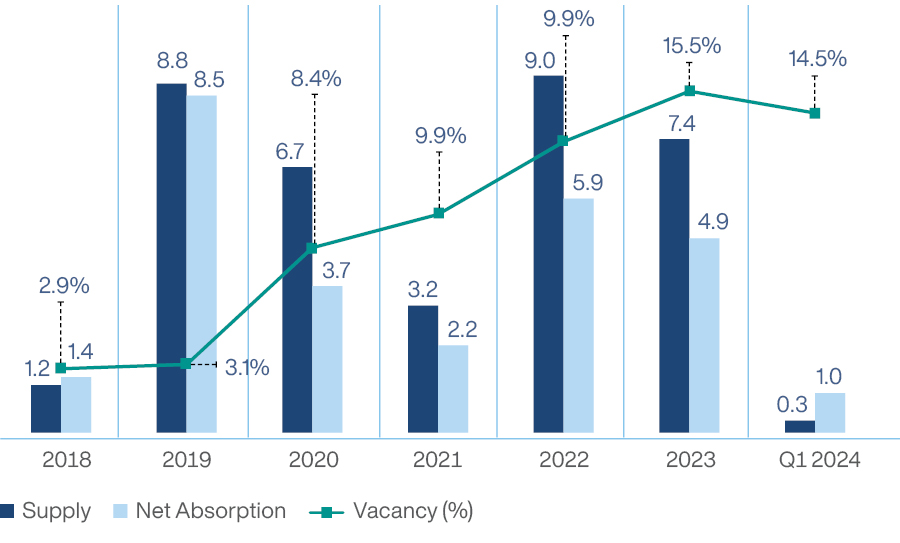

Top seven markets in India comprised c. 794 msf of Grade A completed stock as of March 31, 2024. Mindspace REIT is present in four of the top seven markets (Mumbai Region, Hyderabad, Pune, and Chennai). The net absorption during CY23 stood at c.43 msf, and our micro-markets constituted 59.0% of the net absorption during the year. These cities have exhibited strong underlying growth fundamentals, such as economic and employment growth, diverse pool of tenants, educated workforce, robust transportation infrastructure, and favorable d Office demand recovery emand and supply trends.

c.62 MSF

Gross Leasing in CY23

c.43 MSF

Net Absorption in CY23

Completed Stock for top seven markets (%)

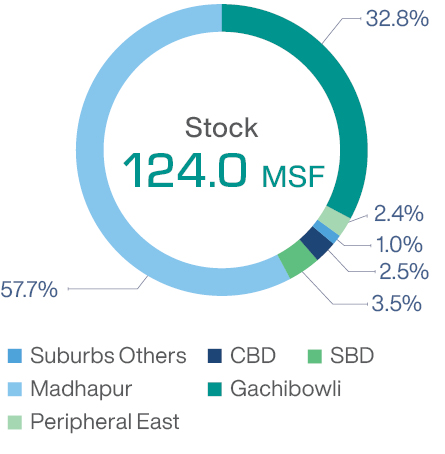

Hyderabad, Telangana's capital, has surged as India's second-largest tech hub, hosting a c.1 million strong tech workforce. The city's GDP is predominantly fueled by its IT/ITeS and pharmaceutical sectors. Initiatives like TS-iPass, Hyderabad's pro-business environment has spurred rapid economic growth over the past five years, attracting both domestic and international investment.

This growth cements Hyderabad's status as a pivotal player in India's tech arena.

Completed Stock in sq ft (%)

Key Updates – Madhapur

Source: Jones Lang LaSelle Inc. (JLL)

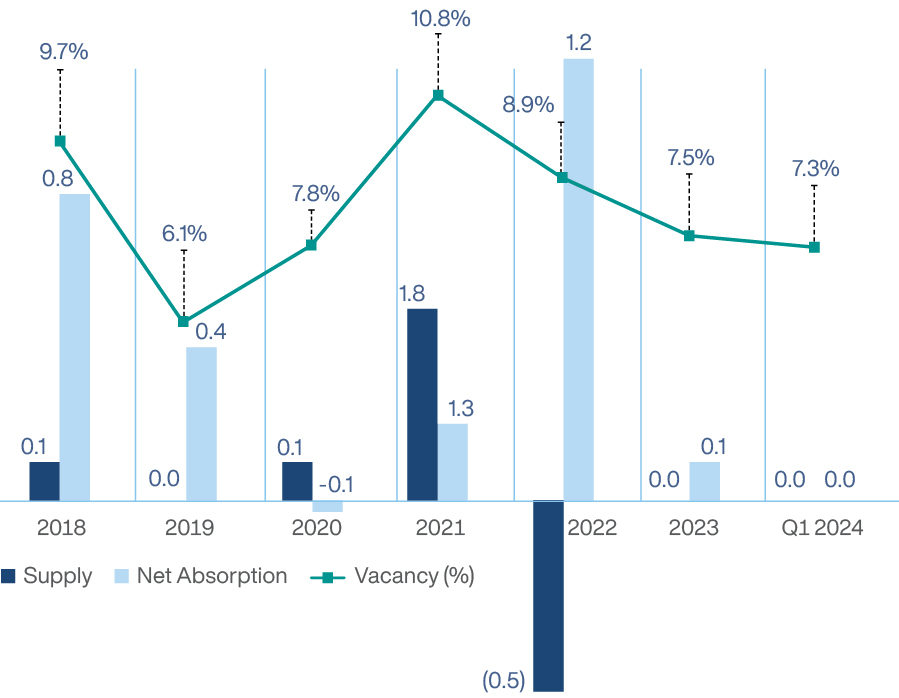

- Madhapur has been the most

sought-after market in Hyderabad

as it enjoys superior connectivity

and well-established infrastructure

in the city

- Leasing activity in Madhapur was

largely driven by IT/ITeS over

the years. However, in the last

couple of years, GCCs from BFSI,

healthcare and flex, telecom firms

have also favored expanding their

operations in the submarket

- Rents in Madhapur have grown at

a CAGR of c.4.3% between 2018

and Q1 2024

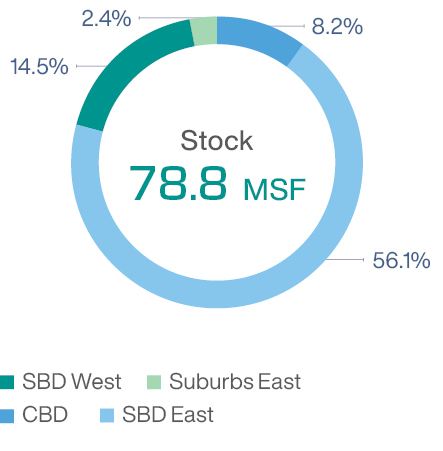

Pune is an important industrial hub having presence of prominent foreign as well as domestic automobile, automobile ancillaries and electronics manufacturers. Attractive demographics and readily available skilled workforce have attracted corporates from various sectors like IT/ITeS, manufacturing/industrial, BFSI, consulting etc., to have their set-up in the city. Other drivers like proximity to Mumbai, good connectivity through air, rail and roads, flow of Foreign Direct Investments (FDIs) have been instrumental in its growth.

Completed Stock in sq ft (%)

Key Updates – SBD East

Source: JLL and Wakefield Research

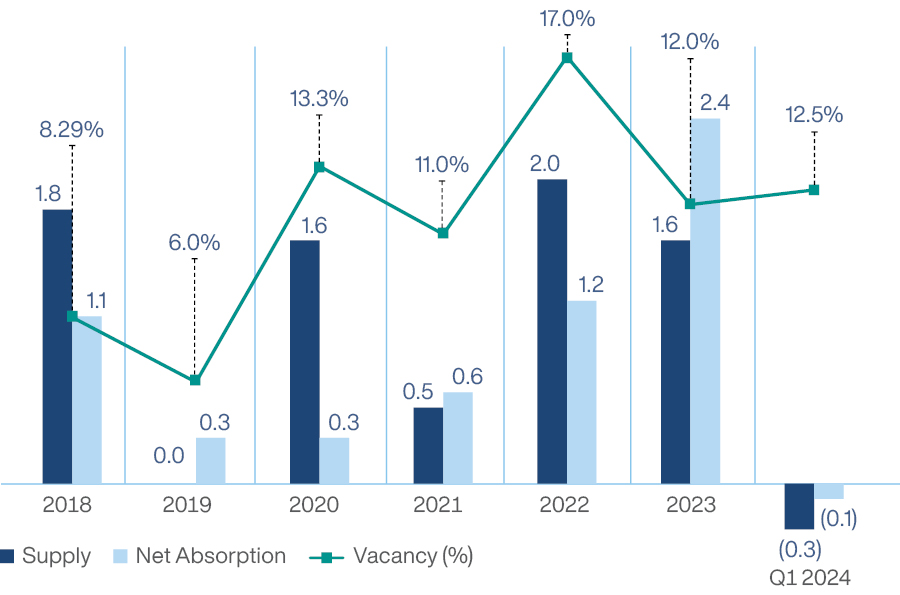

- SBD East has the largest share – c. 56.1% in the total Grade A stock of the city and has accounted for a 56% share of net absorption from CY2019 to Q1 FY24

- SBD East has consistently recorded lower vacancy levels than the city's average. It has highest rentals amongst all the micro-markets in Pune

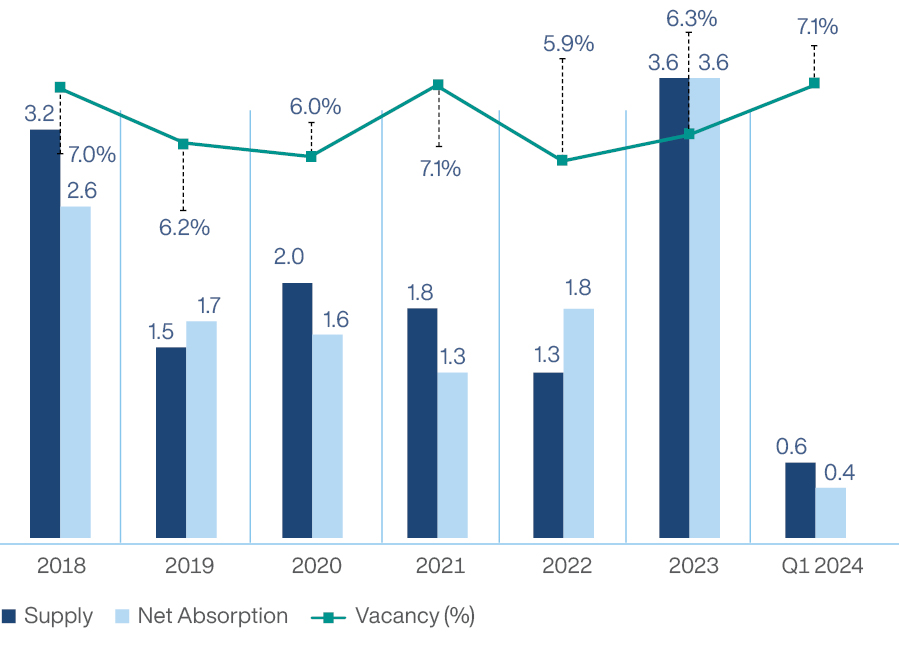

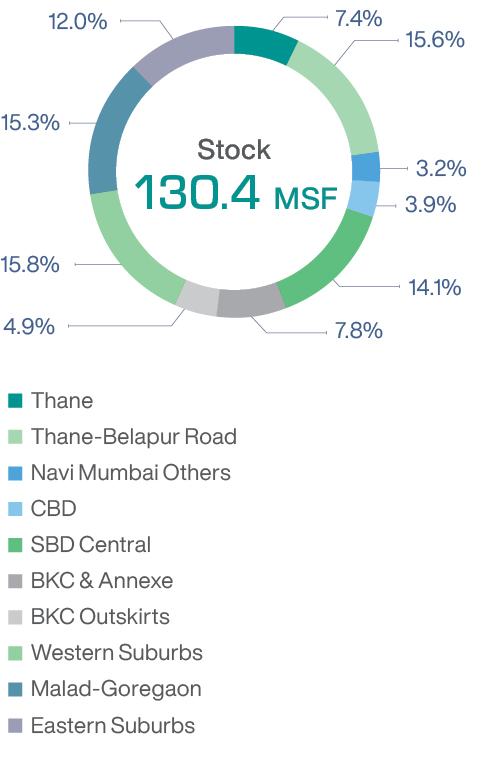

Mumbai is the financial capital, an economic powerhouse, and one of the key industrial hubs of India. It is also one of the most expensive real estate markets in India, with rents and capital values in the key office sub-markets being the highest in the country.

Completed Stock in sq ft (%)

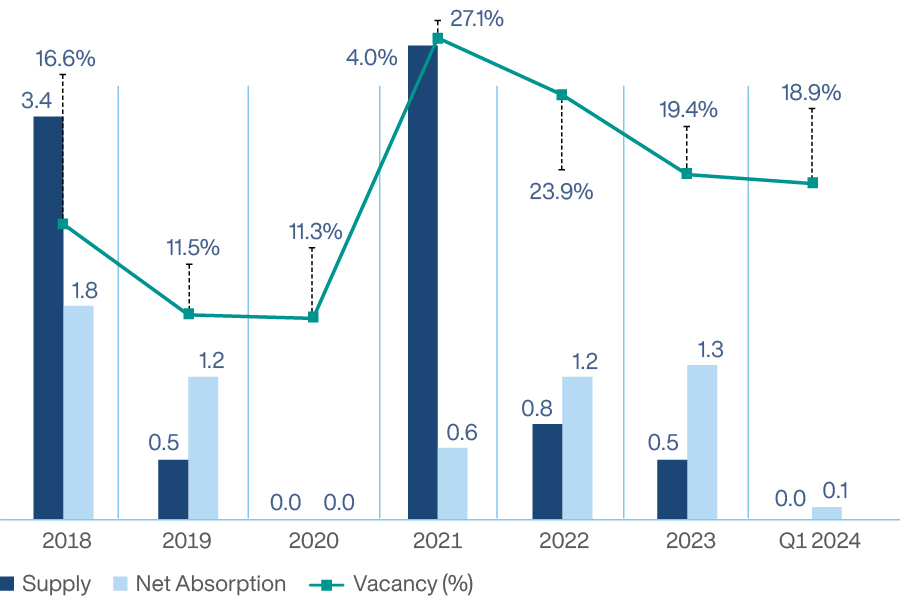

Key Updates - Thane-Belapur Road

Source: Jones Lang LaSelle Inc. (JLL)

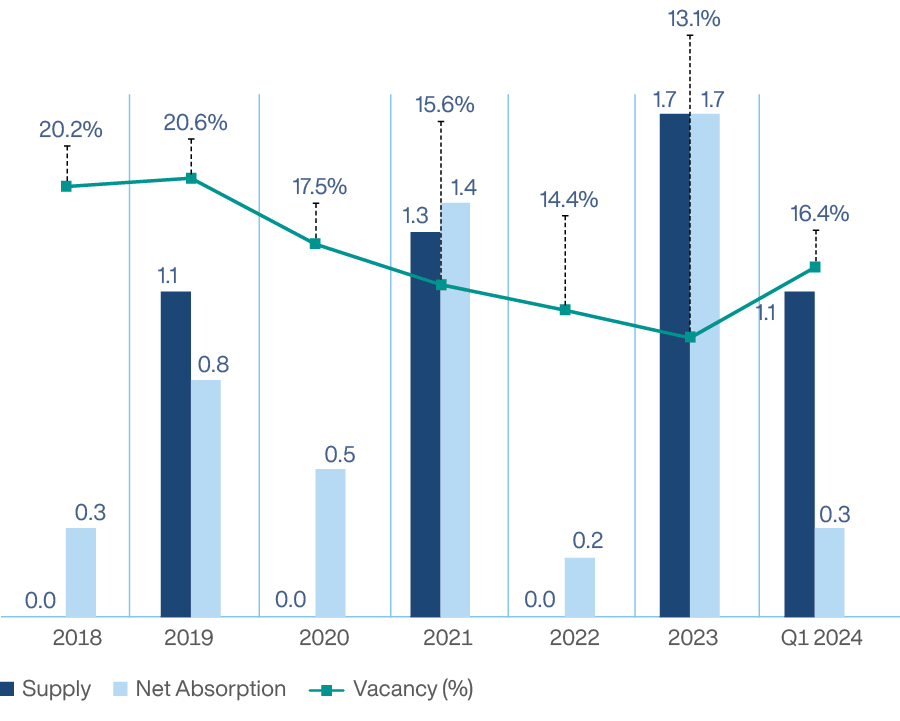

- In the Thane-Belapur market, quality

institutional assets have enjoyed

strong occupancy levels and stratatitled

projects are major contributors

to headline vacancy

- The IT/ITeS tenants accounted for

a major chunk of the leasing activity

in the past five years in the Thane-

Belapur market. Recently, BFSI and

co-working operators have been

quite active

- Thane-Belapur Road has witnessed

strong demand from IT/ITeS

companies and BFSI back offices as

they require larger office spaces at

relatively cheaper rents

- Vacancy in the micro-market is

largely on account of SEZ properties

Key Updates - BKC and Annexe

Source: Jones Lang LaSelle Inc. (JLL)

- BKC and Annexe remains the premier front office submarket in Mumbai

- Limited supply and robust space take-up has ensured that vacancy levels have now dropped down to single digits

and vacancy remains extremely limited in quality assets

Key Updates - Malad-Goregaon

Source: Jones Lang LaSelle Inc. (JLL)

- Quality social infrastructure, improving connectivity through the operational metro lines, and competitive rentals make Malad-Goregaon a major office corridor for global occupiers

- The strong demand and low relevant vacancy have combined to push up the average rents

Chennai is the fourth-largest metropolitan city in India. The rapidly evolving real estate sector is benefiting from the strong growth of the IT and Manufacturing industries and improving infrastructure. The city is culturally diverse and socially cosmopolitan.

Completed Stock in sq ft (%)

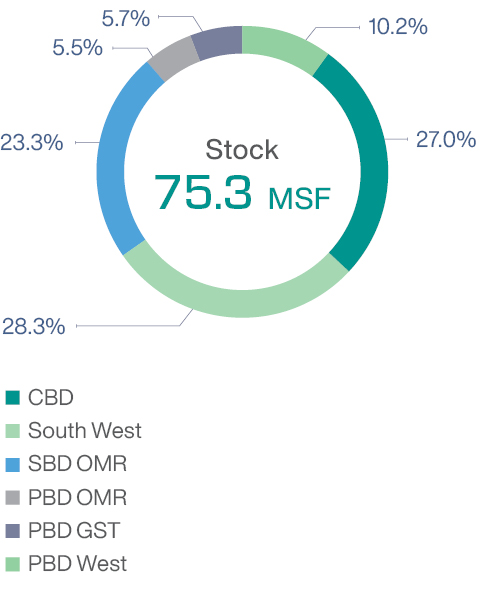

Key Updates – South-West

Source: Jones Lang LaSelle Inc. (JLL)

- The South-West market accounts

for c. 27% share of the operational

Grade A stock in Chennai

- The South-West market has

clocked an average 28% share of

net absorption from CY2019 to

Q1 FY24. In the post-COVID period,

it has recorded highest ever net

absorption in CY2023

- The submarket has been dominated

by Manufacturing/Industrial and IT/

ITeS occupiers in terms of share of

leasing activity, but in more recent

times BFSI occupiers have scaled up

their presence